The way people handle money has changed significantly over the last few years. From buying groceries to paying utility bills, more people now prefer quick and simple digital transactions over carrying physical cash. This growing cashless payment habit change reflects how technology is reshaping everyday financial decisions. Convenience, speed, security, and the rise of smartphone-based payment systems have all contributed to this transformation. As a result, digital payments behavior is becoming a normal part of daily life across all age groups.

Consumers are also noticing how their overall spending trend changes when using digital payment methods. Instant transfers, mobile wallets, UPI systems, and contactless cards make payments faster, but they also influence purchasing decisions. The cashless payment habit change is not just about payment methods—it represents a broader lifestyle shift where financial habits are becoming more connected to technology, convenience, and modern consumer expectations.

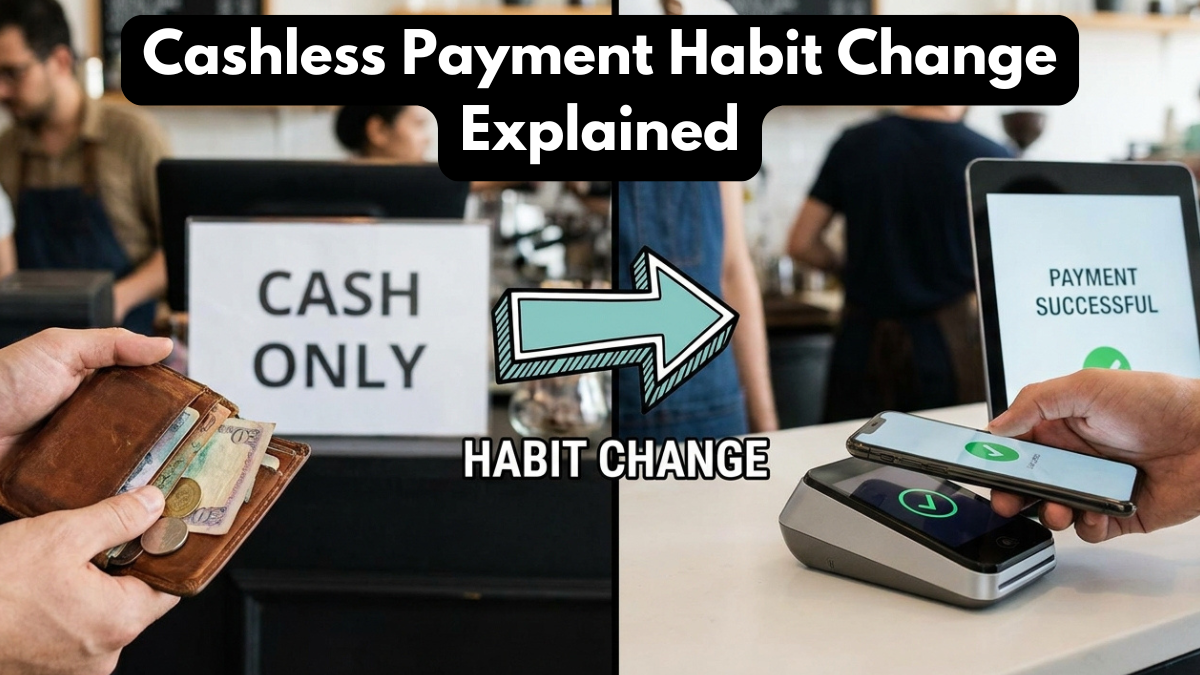

Understanding the Cashless Payment Habit Change

The cashless payment habit change refers to the increasing preference for digital transactions instead of using physical cash for regular expenses. Earlier, cash was seen as the most trusted and convenient form of payment. Today, that idea has changed as online banking and mobile payment systems have become widely accessible.

This shift is strongly linked to evolving digital payments behavior. People now use QR codes, mobile wallets, debit cards, and instant bank transfers for everything from transportation to food delivery. These tools offer speed and flexibility that traditional cash transactions often cannot provide.

At the same time, this transformation also affects the personal spending trend of consumers. Digital transactions create better spending visibility, but they can also encourage faster and sometimes impulsive purchases. This makes the cashless payment habit change both convenient and behaviorally significant.

Why Digital Payments Behavior Is Growing Rapidly

The rise in digital payments behavior is one of the clearest signs of the cashless payment habit change. Several practical reasons explain why people are moving toward cash-free transactions in both urban and rural areas.

Some of the major reasons include:

- Faster payments with no need for exact cash

- Easy bill payments and automatic reminders

- Better transaction tracking through banking apps

- Cashback offers and reward programs

- Safer transactions with reduced cash handling

- Convenience for online shopping and subscriptions

Consumers also trust digital systems more because payment records are easily available. This transparency improves confidence and encourages stronger digital payments behavior over time.

As these services become more user-friendly, the cashless payment habit change continues to grow across different income groups and lifestyles.

Comparison Between Cash Payments and Digital Payments

| Payment Method | Advantages | Challenges |

|---|---|---|

| Cash Payments | Direct control, no technology needed | Harder to track spending, risk of loss |

| Mobile Wallets | Fast, convenient, rewards available | Internet dependency |

| UPI Payments | Instant transfers, simple access | Requires smartphone familiarity |

| Debit/Credit Cards | Accepted widely, secure options | Overspending risk |

This table highlights how the cashless payment habit change is driven by practical benefits that suit modern lifestyles. Convenience often becomes the deciding factor for many consumers.

How Spending Trend Patterns Are Changing

A person’s spending trend often changes once digital payments become part of daily life. When cash is used, spending feels more visible because physical money leaves the hand. With digital payments, transactions happen instantly, often making spending feel less noticeable.

This is one reason why the cashless payment habit change can influence budgeting habits. Some people become more disciplined because banking apps help them monitor expenses clearly. Others may spend more impulsively because quick payments reduce the emotional pause before purchasing.

Modern digital payments behavior has also increased subscription-based spending. Monthly streaming services, automatic bill payments, and app-based purchases are now common parts of personal finance. These patterns show how the spending trend is becoming more automated and less physically controlled.

Financial literacy is therefore becoming more important. Understanding how to manage digital spending helps people benefit from convenience without losing control over expenses.

Business Impact of Cashless Payment Systems

The cashless payment habit change does not affect only consumers—it also transforms how businesses operate. Small shops, restaurants, service providers, and online sellers now rely heavily on digital transaction systems.

Higher digital payments behavior improves sales opportunities because customers prefer flexible payment options. A store that accepts QR payments or contactless cards often creates a smoother buying experience and stronger customer trust.

Business owners can also analyze customer spending trend data more effectively through digital records. This helps with inventory planning, financial forecasting, and customer service improvements.

Even local street vendors now use digital payment platforms, proving how deeply the cashless payment habit change has entered everyday commerce. This shift supports faster economic activity and stronger financial inclusion.

Future of Cashless Transactions

The future strongly supports the cashless payment habit change as technology continues to improve payment systems. Contactless payments, biometric verification, AI-driven fraud detection, and seamless banking integration are making digital finance even more accessible.

As digital payments behavior becomes stronger, future consumers may rely even less on physical wallets and more on mobile-based financial systems. Smartwatches, wearable payments, and voice-assisted banking may further simplify transactions.

The personal spending trend of future generations will likely be shaped by these systems from an early age. Cash may remain important in some areas, but digital transactions will continue leading modern financial habits.

This makes the cashless payment habit change not just a temporary shift, but a long-term evolution in how people interact with money.

Conclusion

The cashless payment habit change reflects the growing connection between technology and everyday financial life. Convenience, speed, and accessibility have made digital transactions a preferred choice for many consumers. Stronger digital payments behavior and changing spending trend patterns show that people are not just changing payment methods—they are changing financial habits.

While digital payments offer many benefits, responsible spending remains important. Understanding personal budgeting, transaction tracking, and spending discipline ensures that convenience does not lead to financial stress. As technology advances, the cashless payment habit change will continue shaping the future of commerce and personal finance.

FAQs

What is the cashless payment habit change?

The cashless payment habit change refers to the growing preference for digital transactions like UPI, cards, and mobile wallets instead of using physical cash.

Why is digital payments behavior increasing?

Digital payments behavior is growing because digital systems offer faster transactions, better convenience, improved safety, and easier spending tracking.

How does spending trend change with digital payments?

The spending trend may become faster and more automated with digital payments, sometimes improving budgeting and sometimes increasing impulsive spending.

Are cashless payments safer than cash?

In many cases, yes. Digital payments reduce physical cash handling and provide transaction records, which improve security and financial transparency.

Will cash disappear completely in the future?

Cash may still remain important in some situations, but the cashless payment habit change shows that digital transactions will continue becoming the dominant payment method.

Click here to learn more